Rupee Depreciation: Structural Weaknesses vs Global Factors

|

Getting your Trinity Audio player ready...

|

PERSPECTIVE ANALYSIS

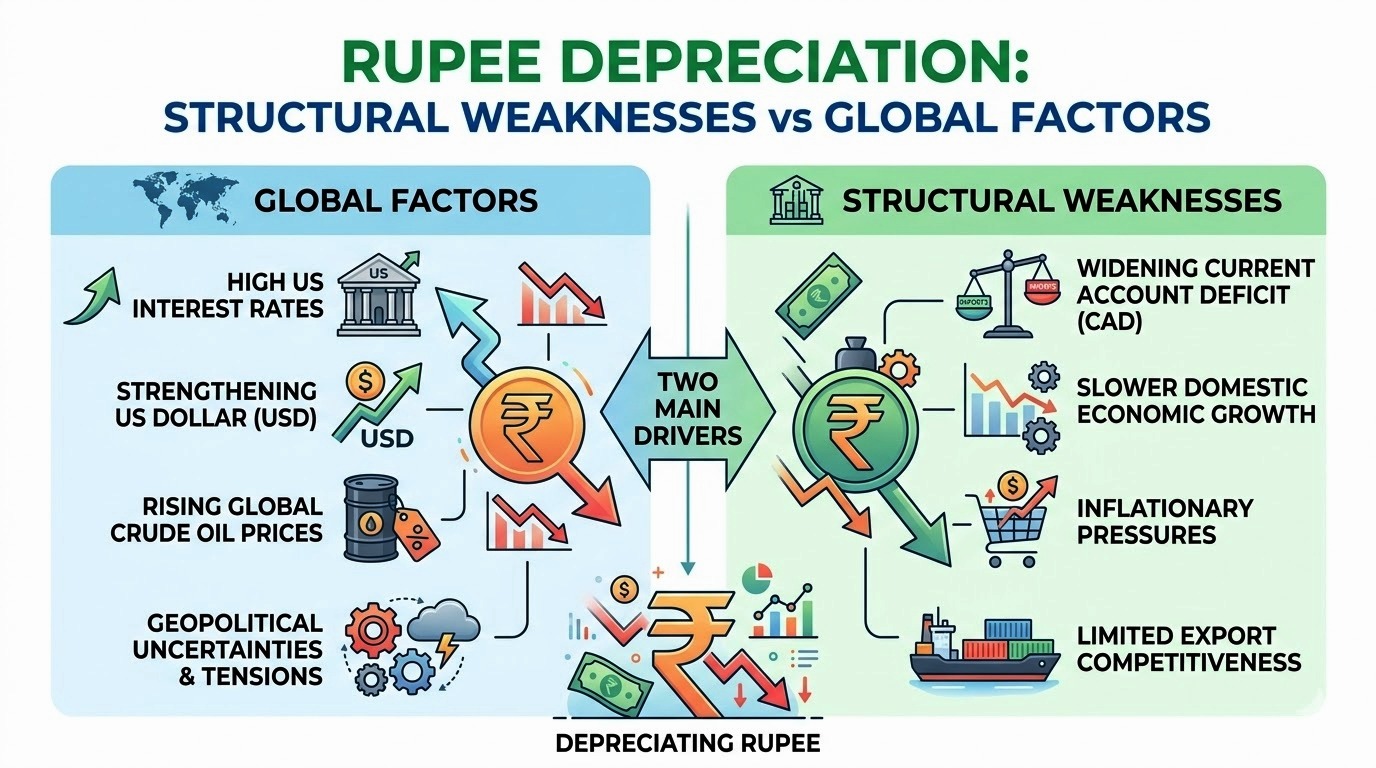

The Indian Rupee (INR) has entered a phase of historic volatility in early 2026, recently hitting a record low of ₹94.12 per US Dollar in late March before hovering around the ₹93.8 mark in April. This downward trajectory has sparked a critical debate among economists and policymakers: is the Rupee’s decline a result of unavoidable global headwinds, or does it expose deep-seated structural flaws within the Indian economy? To navigate this issue, one must analyze the interplay between external shocks and internal imbalances.

Global Factors: The External Onslaught

In the first half of 2026, the global macroeconomic landscape has been defined by a perfect storm of geopolitical friction and monetary tightening, both of which have been hostile to emerging market currencies.

Geopolitical Turmoil and the Energy Shock: India’s heavy reliance on energy imports remains its primary external vulnerability. In early 2026, escalating tensions in West Asia specifically maritime disruptions in the Strait of Hormuz sent crude oil prices surging. For a country that imports over 85% of its crude requirements, such supply shocks lead to imported inflation. The necessity to purchase increasingly expensive oil creates a massive demand for Dollars, naturally exerting downward pressure on the Rupee.

The US Federal Reserve’s Higher for Longer Stance: Contrary to earlier expectations of aggressive rate cuts, the US Federal Reserve maintained interest rates in the 3.5–3.75% range through early 2026 to combat persistent US inflation. This has sustained the Greenback’s strength. As US yields remain attractive, global capital particularly Foreign Portfolio Investment (FPI) has flowed back to safe-haven US assets. In India, this was reflected in significant sell-offs in the domestic equity market and a sharp withdrawal of foreign capital in April 2026, further weakening the INR.

Global Trade Protectionism: The 2026 trade environment is increasingly fragmented. New tariffs, including a 10% duty on certain Indian goods imposed by the US following recent legal disputes, have hampered export growth. While a weaker Rupee usually makes exports cheaper, global demand slowdowns have neutralized this advantage, leaving the trade balance in a precarious state.

Structural Weaknesses: The Domestic Underpinnings

While global factors provide the immediate trigger, India’s internal structural framework determines the currency’s long-term vulnerability.

Persistent Merchandise Trade Deficit: Despite reaching a service export surplus, India suffers from a chronic merchandise trade deficit. Although the trade gap narrowed to $20.67 billion in March 2026 (the smallest since June 2025), the underlying trend remains one of heavy dependence on imported electronics, machinery, and gold. This structural gap creates a permanent deficit that must be financed by capital inflows, making the Rupee hypersensitive to the whims of global investors.

Reliance on Volatile Hot Money: A major structural weakness is the composition of India’s capital account. While Foreign Direct Investment (FDI) is stable and long-term, India still relies heavily on FPIs to bridge its Current Account Deficit (CAD). FPIs are mercurial, they flee at the first sign of global risk. The April 2026 depreciation was directly correlated with FPI outflows as investors sought refuge from West Asian uncertainties.

Inflation Differentials and PPP: According to the principle of Purchasing Power Parity (PPP), a currency with higher domestic inflation relative to its trading partners will eventually depreciate. India’s recent struggle with supply-side food inflation and high fuel costs has kept its inflation rate higher than that of the US or EU, exerting a long-term devaluation pull on the Rupee’s real effective exchange rate (REER).

Interplay, Impacts, and Policy Response – My Opinion

The two sets of factors are not mutually exclusive; global hit hardest where structures are weakest. Elevated oil prices from geopolitics widen the CAD precisely because of energy dependence. FPI outflows accelerate when domestic inflation differentials signal policy divergence. The RBI has responded adeptly: intervening via dollar sales (reserves dipped from a $728 billion peak but rebounded to approximately $701 billion by mid-April 2026), imposing temporary bank exposure caps, and allowing orderly depreciation to preserve buffers. Reserves still cover over 10–11 months of imports, a comfortable cushion.

Economically, depreciation is a double-edged sword. It boosts exporters, remittances, and tourism receipts while making Indian assets cheaper for foreign buyers. However, it fuels imported inflation (oil and electronics constitute a large import bill), erodes purchasing power, and raises the cost of external debt servicing. For a consumption-driven economy, this can dampen growth if unchecked. Net trade gains are often muted due to high import intensity in exports.

Strategic Depreciation: A Hidden Advantage?

Some analysts argue that the current depreciation is a “correction” rather than a crisis. With the IMF projecting India to temporarily slip to the 6th largest economy in 2026 due to exchange rate fluctuations, a slightly weaker Rupee may actually be a strategic necessity. It helps offset the impact of global tariffs and maintains the competitiveness of Indian labour in the global ‘China Plus One’ manufacturing shift. The Economic Survey 2025-26 suggests that growth, driven by domestic demand and infrastructure projects like Gati Shakti, remains the priority over a “strong” but uncompetitive currency.

Stability, Policy Imperatives and Outlook

Looking ahead, the rupee’s trajectory will hinge on global stabilisation easing oil prices, Fed pivot, or de-escalation in West Asia coupled with domestic resolve. Short-term management via RBI tools is effective, but sustainable strength demands structural overhaul: accelerating renewable energy and domestic oil exploration to curb energy imports; deepening manufacturing via targeted reforms and trade agreements; enhancing export quality and diversification; and maintaining fiscal prudence to widen growth-interest differentials favourably.

For long-term stability, India must focus on three pillars:

- Energy Transition: Reducing the oil import bill through green hydrogen and geothermal energy.

- Export Diversification: Moving from services to high-value manufacturing to narrow the trade gap.

- Deepening Financial Markets: Attracting long-term debt capital to reduce the impact of equity market volatility.

Ultimately, the Rupee’s value is a reflection of the nation’s economic health. While the current volatility is a test of resilience, India’s robust growth fundamentals and massive forex reserves suggest that while the Rupee may be bending under global pressure, it is far from breaking.