Challenges of Forex Reserves in India

|

Getting your Trinity Audio player ready...

|

PERSPECTIVE ANALYSIS

Foreign exchange (forex) reserves serve as the premier economic firewall for an emerging market economy. For India, a nation deeply integrated into global trade and capital workflows, these reserves managed by the Reserve Bank of India (RBI) represent more than mere financial savings; they are an instrument of strategic sovereignty, monetary stability, and geopolitical leverage. Historically haunted by the 1991 Balance of Payments (BoP) crisis, where reserves plummeted to less than three weeks of import cover, India has consciously built a massive forex buffer over the subsequent decades.

By the mid-2020s, India’s forex reserves reached historic milestones, comfortably crossing the $700 billion threshold. This quantitative milestone places India among the top global holders of foreign currency liquidity alongside China, Japan, and Switzerland, providing an enviable cushion against external economic shocks.

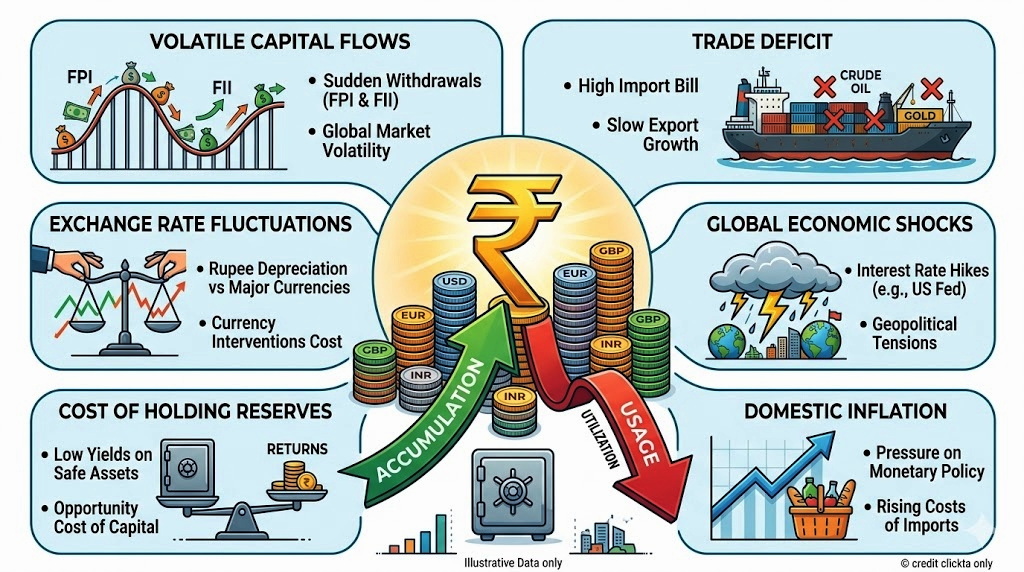

However, looking past the impressive headline figures reveals a complex web of structural challenges. The contemporary macroeconomic environment has fundamentally altered the costs, dynamics, and safety of maintaining such large reserves. From the structural vulnerability of capital inflows to the fiscal drag of sterile assets, India’s current forex landscape presents a complex paradox: a fortress of safety built on highly volatile foundations.

Composition of India’s Forex Architecture

To evaluate the challenges associated with India’s current forex position, one must understand how these funds are allocated. The RBI categorizes its reserves into four distinct components, each carrying unique management mandates:

Foreign Currency Assets (FCA)

The dominant component of the reserve basket, FCA comprises investments in multi-currency assets. It is heavily weighted toward the US Dollar, followed by the Euro, the British Pound, and the Japanese Yen. These assets are primarily parked in sovereign bonds and institutional deposits overseas.

Gold Reserves

Acting as a traditional hedge against inflation, currency devaluation, and sovereign default risk, gold has witnessed strategic accumulation by the RBI over the last several years to diversify away from fiat currency volatility.

Special Drawing Rights (SDRs)

An international reserve asset created by the International Monetary Fund (IMF) to supplement its member countries’ official reserves.

Reserve Position in the IMF

The quota-based financial claim held by India within the IMF, which can be drawn upon during periods of extreme macroeconomic stress.

While this diversification provides a multi-layered safety net, the management, valuation, and return profile of these specific components form the center of contemporary policy friction.

The Primary Dilemma

The most glaring structural vulnerability of India’s forex reserves lies in how they are accumulated. Broadly, a nation can earn foreign exchange through two pathways: an earned Current Account Surplus (exporting more goods and services than it imports) or a borrowed Capital Account Surplus (attracting foreign investments, external loans, and banking capital).

Unlike export-driven powerhouses like China, Taiwan, or the Eurozone nations, India consistently runs a structural Current Account Deficit (CAD). This deficit is driven by an insatiable domestic demand for imported crude oil, electronic hardware, weapon systems, pulses, and gold. Consequently, India’s forex reserves are not surplus earnings from trade; they are built almost entirely on capital inflows. This reliance introduces a high degree of vulnerability through two main transmission channels.

The Hot Money Dilemma

A significant portion of India’s capital inflows consists of Foreign Portfolio Investment (FPI) in the debt and equity markets. FPIs are highly sensitive to global interest rate differentials, geopolitical risks, and shifting global risk appetites. When the US Federal Reserve or the European Central Bank alters its monetary policy trajectory, or when global geopolitical tensions flare up, these funds can exit the domestic market overnight. This leaves the RBI vulnerable to sudden capital flight, transforming a seemingly stable multi-hundred-billion-dollar buffer into a volatile shield during global market panics.

The Structural Debt Component

The capital account is further populated by Non-Resident India (NRI) deposits and External Commercial Borrowings (ECBs) raised by Indian corporates. These are debt liabilities that carry explicit servicing costs and fixed maturities. Accumulating reserves via debt means the nation is essentially paying an interest premium to borrow foreign funds, only to park them in low-yielding safe-haven assets abroad. This creates an unstated structural tax on the broader economy.

The Microeconomics of Reserves

Holding large amounts of foreign currency assets is far from cost-free. In central banking economics, this challenge manifests through two interconnected phenomena: the Cost of Carry and Monetary Sterilization.

The Opportunity Cost and Yield Mismatch

The bulk of India’s Foreign Currency Assets is invested in highly liquid, top-tier sovereign paper, predominantly US Treasury bills. These instruments offer relatively low yields compared to the domestic cost of capital in India. When the RBI buys foreign currency inflows to build reserves, it issues domestic currency (Rupees) into the banking system.

The cost of this domestic liquidity (reflected in domestic interest rates) is generally much higher than the nominal returns earned on US or European bonds. This negative yield spread constitutes a direct financial drain, often termed the negative cost of carry, which impacts the central bank’s balance sheet and potential dividend payouts to the government.

The Sterilization Dilemma

When the RBI purchases incoming foreign exchange to build reserves and prevent the Rupee from appreciating excessively, it injects fresh liquidity into the domestic banking system. If left unmanaged, this sudden expansion of base money can fuel domestic inflationary pressures, asset bubbles, and distort credit growth.

To counter this, the RBI must perform Sterilization Operations. It absorbs the excess domestic liquidity by selling government securities through Open Market Operations (OMO) or using tools like the Market Stabilization Scheme (MSS).

This dynamic introduces clear domestic trade-offs: it reduces the RBI’s holding of yield-earning domestic government bonds, and it maintains upward pressure on domestic interest rates, which can unintentionally crowd out private capital expenditure and raise borrowing costs for domestic enterprises.

The Intervention Paradox of Defending Rupee vs. Reserve Depletion

The primary operational mandate of the RBI’s forex management is to prevent excessive volatility in the Indian Rupee (INR). The RBI does not explicitly target a specific exchange rate value, but it steps in heavily to ensure orderly market conditions and prevent speculative attacks on the currency.

When global shocks such as energy supply disruptions or sudden monetary tightening in developed markets trigger a sell-off in emerging market currencies, the RBI must step into the spot and forward currency markets. It sells US dollars and buys rupees to cushion the domestic currency’s fall.

While this intervention successfully stabilizes the rupee in the short term, protecting the domestic macroeconomic environment from destructive imported inflation, it can lead to rapid and alarming drawdowns of the reserve cushion during extended periods of global volatility. Past macroeconomic cycles have demonstrated that defensive interventions can burn through tens of billions of dollars within a few quarters. This highlights the continuous friction between maintaining a headline grabbing reserve figure and executing exchange rate management.

Geopolitical Vulnerabilities and the De-Dollarization Imperative

The modern global financial architecture has evolved in a way that introduces non-traditional, systemic risks to reserve management. The freezing of Russia’s foreign exchange reserves following geopolitical conflicts demonstrated that large forex reserves held in Western central banks or cleared through Western payment networks carry clear counterparty risks. While India maintains an independent, strategic, and balanced foreign policy, the structural concentration of its forex assets in US Dollar-denominated assets exposes it to two distinct vulnerabilities:

Valuation Shocks

Because forex reserves are reported globally in US Dollar terms, any fluctuation in the value of the greenback relative to other global reserve currencies (such as the Euro, Pound Sterling, or Japanese Yen) creates accounting volatility. When the US dollar strengthens globally, the non-dollar portion of India’s assets automatically depreciates in dollar terms, leading to multi-billion-dollar valuation losses on paper without any actual capital outflow taking place.

De-Dollarization and Diversification Imperatives

The global shift toward a multipolar financial world places pressure on the RBI to diversify away from the US Dollar. However, alternative avenues present their own structural bottlenecks. Increasing holdings in Euros or Yen offers very low or negative inflation-adjusted returns, while integrating alternative emerging market currencies is complicated by capital controls and geopolitical friction.

Even expanding gold holdings a strategy the RBI has steadily and wisely pursued presents physical security, transport, storage, and immediate liquidity constraints during sudden, fast-moving balance-of-payments emergencies.

Strategic Energy Imperatives and Structural Outflows

As India positions its economy for the next decade, its forex management is intimately tied to two critical transitions: energy security and technological sovereignty. These priorities require significant capital deployment, altering how reserves must be viewed.

The Hydrocarbon Strain

India remains structurally dependent on imported crude oil and natural gas to fuel its economic engine, importing over 80% of its requirements. Geopolitical flare-ups in critical choke points, such as the Strait of Hormuz or the Red Sea, instantly spike global energy prices. Because oil is heavily priced in dollars, these supply shocks trigger immediate, massive structural drawdowns on India’s forex reserves just to keep the domestic economy running.

Financing the Green Transition

Simultaneously, India’s domestic policy shifts such as its aggressive push toward geothermal energy, green hydrogen, and advanced electronics manufacturing require heavy upfront imports of specialized equipment, rare earth elements, and lithium-ion or solid-state battery technologies.

This structural shift requires policy thinkers to view forex reserves not just as an emergency liquidity cushion, but as a strategic fund capable of enabling technology transfers and securing overseas critical mineral assets.

Strategic Alternatives and Policy Recommendations

Addressing the vulnerabilities inherent in India’s forex architecture requires shifting focus from raw volume expansion to structural quality management and systemic insulation.

Transitioning Inflow Architecture: India must accelerate deep-tier structural reforms to transition portfolio flows- hot money into long-term, stable Foreign Direct Investment (FDI) in manufacturing, infrastructure, and green technology. FDI is far less prone to sudden reversals during global panics.

Addressing the Structural Trade Deficit: The ultimate solution to reserve vulnerability is narrowing the Current Account Deficit. Enhancing domestic manufacturing capabilities through refined Production Linked Incentive (PLI) schemes and accelerating the energy transition to renewables and green hydrogen will structurally reduce the nation’s inelastic import bill.

Promoting Local Currency Settlement (LCS): Expanding bilateral rupee-denominated trade settlement mechanisms with major trading partners, especially for energy imports, allows India to bypass the need for dollar mediation entirely, reducing the transactional demand on the central forex pool.

Dynamic Asset Diversification: The RBI should continue its strategic shift toward building up physical gold reserves and exploring highly rated multilateral development bank bonds, balancing the traditional need for liquidity with modern requirements for geopolitical safety and inflation hedging.

Balancing Safety with Progress

India’s large foreign exchange reserve is an undeniable monument to its post-1991 macroeconomic resilience, providing a vital shield against external economic disruptions. Yet, maintaining a massive reserve buffer is not a cost-free achievement; it is a defensive tool that comes with real financial trade-offs, structural strains, and sterilization costs. The core challenge for India’s policymakers is that these reserves are built on volatile capital inflows rather than a structurally sound trade surplus. Moving forward, India’s long-term economic sovereignty will depend less on the total size of its central bank reserves and more on its ability to fix structural trade imbalances, reduce import dependence on energy, and convert volatile capital inflows into long-term investments in the domestic economy.

Ultimately, the strongest shield for the Rupee is not an ever-expanding stockpile of foreign debt securities, but a highly competitive, self-sustaining, and structurally balanced domestic economy.