Hormuz Crisis and India’s Energy Security Challenge

|

Getting your Trinity Audio player ready...

|

EXPLAINER

What is India’s total Energy Consumption?

Electricity Consumption & Power Demand

In the fiscal year just concluded (FY 2025–26), India’s power sector reached historic peaks.

- Total Annual Generation (FY 2025–26): 1,845.9 Billion Units (BU).

- Peak Power Demand Met: 242.49 GW (met in June 2025). The CEA projects peak demand to rise to 289 GW for the upcoming 2026–27 cycle.

- Per Capita Consumption: Surged to 1,460 kWh (as of end-2025), a ~53% increase over the last decade.

- Energy Deficit: Reduced to a near-negligible 0.03%, indicating that total consumption is now almost equal to total demand.

Petroleum & Natural Gas Consumption

The most recent data from the PPAC (Monthly Ready Reckoner) for the period ending March 31, 2026, shows robust growth in hydrocarbon demand despite the Hormuz crisis.

| Fuel Category | Consumption (February/March 2026) | Growth (YoY) |

| Total Petroleum Products | 20.24 MMT (monthly avg) | +4.7% |

| Diesel (HSD) | 7.66 MMT | +4.3% |

| Petrol (MS) | 3.37 MMT | +6.1% |

| LPG (Domestic) | 2.82 MMT | +9.3% |

| Aviation Fuel (ATF) | 764 TMT | +4.0% |

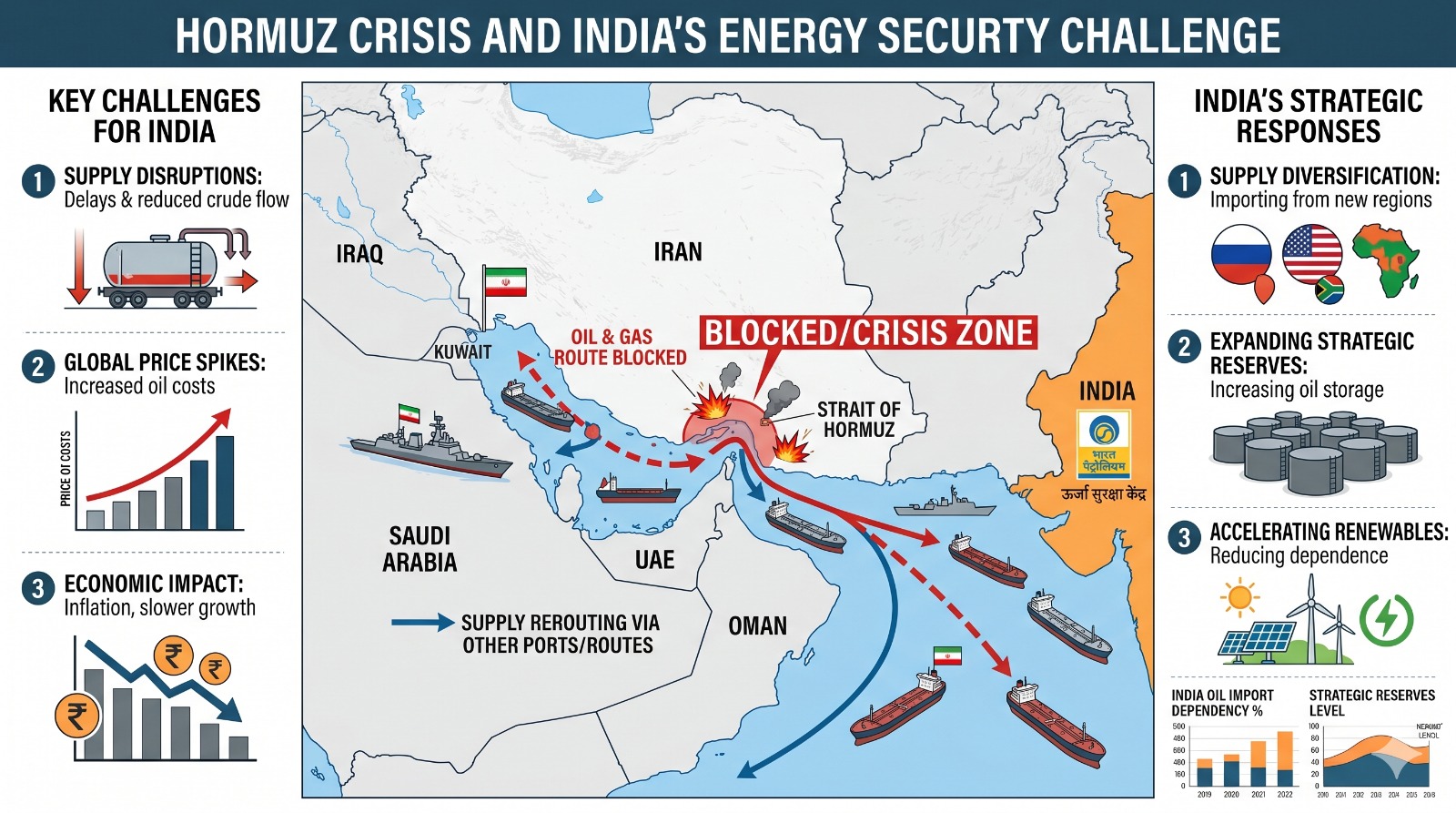

Why is the Strait of Hormuz so critical for India’s energy security?

The Strait of Hormuz is a narrow maritime chokepoint (widest point ~33–39 km) between Iran and Oman, linking the Persian Gulf to the Gulf of Oman and Arabian Sea. It serves as the world’s most critical energy transit route, carrying nearly 21 million barrels per day (mb/d) of oil and petroleum products about one-fifth (20–25%) of global seaborne oil trade plus significant volumes of LNG. Roughly 80% of this flow heads to Asia.

For India the world’s third-largest crude oil importer and consumer (daily consumption ~5.3–5.6 million barrels) the strait is vital because the country imports 85–88% of its crude oil needs. Disruptions here directly threaten supply stability, affordability, and broader economic security.

Even with diversification efforts, a substantial portion of India’s energy supplies physically passes through or depends on this route:

Crude Oil: As of March–April 2026, ~30–40% of India’s crude imports transit the Strait of Hormuz (down from ~45–50% earlier due to rerouting). Gulf suppliers (Saudi Arabia, Iraq, UAE, Kuwait) remain key sources. India sources crude from 40+ countries, with ~70% now routed via alternative paths (e.g., Russia, West Africa, US, Latin America). However, global price spikes from any disruption affect all imports.

LPG (Liquefied Petroleum Gas — primary cooking fuel for ~330 million households): India imports ~60% of its LPG consumption. ~90% of these imports (mainly from the Middle East/Gulf) pass through the Strait of Hormuz. This makes LPG the most vulnerable segment, with recent disruptions causing sharp drops in arrivals (e.g., ~46% lower in March 2026).

LNG (Liquefied Natural Gas): Over 50–60% of India’s LNG imports transit the strait, largely from Qatar (~40% of total LNG supplies). LNG supports power generation, fertilizers, and industry.

How is India bypassing the Hormuz disruption?

To bypass the April 2026 Hormuz disruption, India has moved from a Gulf-centric procurement model to a Multi-Polar Logistics strategy. This involves a combination of naval escorts, diplomatic back-channels, and aggressive trade rerouting.

The current strategy is built on three pillars:

- Operation Sankalp 2.0 (Safety Corridor): The Indian Navy has significantly scaled up Operation Sankalp to manage the blockade. As of April 2026, the strategy is not to challenge the blockade but to secure a humanitarian and energy window for Indian-flagged vessels.

Naval Escorts: The Navy has deployed over half a dozen warships (including logistics support vessels) to the Gulf of Oman. These vessels provide a security corridor for Indian tankers, such as the Shivalik, which successfully delivered the first post-blockade LPG cargo to Mundra Port on March 16.

Diplomatic Immunity: Unlike the US or Israel, India has maintained a Friendly Nation status with Tehran. Iranian authorities have formally signalled safe passage for India-bound vessels, provided they are coordinated through the Indian Navy.

- Massive Market Rerouting (The 70% Shift)

India has drastically reduced the percentage of its oil that must cross the Strait of Hormuz by leveraging global supply gluts and temporary sanctions waivers.

The Russian Pivot: India remains a top buyer of Russian crude, importing roughly 1.15 million barrels per day (bpd) in early 2026. This oil travels via the Red Sea or around the Cape of Good Hope, completely bypassing Hormuz.

Non-Gulf Procurement: Sourcing from the US, West Africa, and Latin America has surged. In 2025, “non-strait” sources accounted for 60% of India’s oil; by March 2026, this has been pushed to 70%.

Sanctions Flexibility: On March 31, 2026, the US Treasury issued a 30-day waiver specifically for Indian refiners to process and discharge Russian crude already in transit, ensuring no sudden supply drop during the height of the Hormuz crisis.

- Inventory Drawdown: The Nine-Day Buffer

India is currently tapping into its strategic and commercial reserves to prevent domestic rationing.

SPR Utilization: India’s Strategic Petroleum Reserves (SPR) in Visakhapatnam, Mangaluru, and Padur currently hold 3.37 million metric tonnes (MMT)—about 63% of their total 5.33 MMT capacity.

Total Cover: While the SPR provides only 9.5 days of cover, the government is coordinating with state-run companies (IOC, BPCL, HPCL) to utilize their commercial stocks. Combined, India currently holds a total petroleum buffer of roughly 60 to 74 days.

If the Strait of Hormuz crisis continues, what will be the broader risks to Indian energy security?

If the Strait of Hormuz crisis which escalated into an effective closure by March 2, 2026 continues unabated, India faces a systemic risk that transcends simple fuel shortages. The crisis has already pushed Brent crude to $126/bbl (as of March 2026) and triggered a US naval blockade on April 13, 2026.

Beyond the immediate price spikes, the broader risks to India’s energy and national security are detailed below:

- LPG & LNG Vulnerability: While crude oil can be rerouted from Russia or the US, LPG (Cooking Gas) and LNG are structurally tied to the Gulf.Household Impact: India imports ~90% of its LPG through Hormuz. As of April 2026, roughly 54% of all Indian households depend on gas that passes through this single chokepoint.

No Strategic Buffer: Unlike crude oil, India has no significant Strategic LPG Reserves. A prolonged crisis could move the country from panic buying (reported in Delhi and Kerala in March) to a complete national dry-out of cooking gas.

Industrial Shutdowns: Under the Essential Commodities Act (invoked March 10, 2026), the government has already capped gas supplies to manufacturing and industrial consumers at 80%, threatening industrial output and employment.

- The Agriculture Food Security Threat

The energy crisis is rapidly morphing into a food security crisis due to India’s reliance on the Middle East for Fertilizers.

Input Scarcity: Roughly 40% of India’s fertilizer imports come from the Middle East. Urea prices have already surged 35% since the conflict began.

The Kharif Risk: The April 2026 blockade coincides with the start of the Kharif (monsoon) planting season. Shortages in urea and ammonia threaten crop yields for rice, pulses, and oilseeds, potentially triggering double-digit food inflation.

DEBATE

Hormuz Crisis and India’s Energy Security Challenge

Debate on the Motion: “A blockade of the Strait of Hormuz creates a critical energy security emergency for India”

(As of April 14, 2026 – Ongoing disruptions from US naval enforcement and Iranian responses have significantly reduced tanker traffic through the Strait)

Thesis Statement

A prolonged blockade of the Strait of Hormuz does create a critical energy security emergency for India, even with substantial diversification of crude oil sources. While ~70% of crude imports now bypass the strait and short-term buffers (around 60 days) provide some cushion, severe vulnerabilities persist in LPG (nearly 90% of imports via Hormuz / Middle East routes), LNG supplies, under-filled Strategic Petroleum Reserves (SPR at ~64% capacity, offering limited dedicated cover), and broader macroeconomic risks including inflation spikes, rupee depreciation, and fiscal strain.

Side I: It Creates a Critical Emergency

Opening Statement: The current 2026 disruptions triggered by US actions targeting Iran-linked shipping and Iranian retaliatory measures have already caused sharp drops in tanker traffic, LPG arrivals (down significantly), and global price volatility, directly exposing India’s structural weaknesses.

Arguments:

- High Vulnerability in LPG and Refined Products

India imports ~60% of its LPG consumption, with nearly 90% of these imports passing through the Strait of Hormuz (primarily from Gulf suppliers). Disruptions have led to notable pressure on supplies for over 330 million households, with risks of shortages in cooking gas and impacts on commercial sectors. Refined product markets are even more exposed than crude, with additional 20–25% exposure in fertilizer supply chains.

- Limited Strategic Buffers

India’s SPR capacity is 5.33 million metric tonnes (MMT) across facilities in Visakhapatnam, Mangaluru, and Padur. As of March 2026, stocks stand at ~3.37–3.372 MMT (~64% full), providing roughly 5–9.5 days of dedicated emergency cover at full capacity. Total national buffer (SPR + commercial stocks) is estimated at ~60–74 days, falling short of the IEA’s 90-day recommendation. Government assurances rely on rerouting, but logistics and insurance risks limit reliability in a full blockade.

- Macroeconomic and Social Ripple Effects

Moody’s has warned that India would bear the maximum brunt among large Asian importers, with risks of higher inflation (potentially above 4.5%), rupee weakening (USD/INR possibly toward 95+), widened current account deficit, and increased subsidy burdens. Every sustained $10/bbl oil price rise can reduce GDP growth by 0.1–0.2 percentage points while adding to inflation. Prolonged disruption could trigger social concerns over cooking fuel and food prices.

Conclusion: Crude diversification helps, but LPG/LNG dependence and thin reserves turn a geopolitical event into a genuine supply and economic emergency.

Side II: It Is a Manageable Challenge, Not a Critical Emergency

Opening Statement: India’s diversification strategy has built meaningful resilience. The 2026 crisis is being navigated without collapse, validating proactive hedging rather than exposing fatal flaws.

Arguments:

- Successful Crude Oil Diversification

As of March–April 2026, India sources crude from 40+ countries, with ~70% of imports routed via alternative paths (up from ~55% previously). Russia’s share has rebounded sharply (potentially reaching 40% during the crisis, supported by a US 30-day waiver), and the Petroleum Ministry states India is receiving more crude overall than pre-disruption levels through diversified suppliers.

- Existing Buffers and Adaptive Response

Total reserves (SPR + commercial) offer a 60–74 day cushion. The government has implemented contingency plans, diplomatic efforts for safe passage, naval coordination, and successful transits of Indian vessels (including LPG carriers). No widespread shortages have occurred, and public measures aim to maintain stability.

- Long-Term Resilience Gains

The crisis is accelerating renewables, green hydrogen, domestic exploration, and SPR Phase-II expansion (targeting additional capacity to reach 11.83 MMT). It demonstrates the effectiveness of multi-supplier hedging in an interconnected world, where complete insulation from chokepoints is unrealistic.

Conclusion: Challenges, especially in LPG, are real but being actively managed. This is a serious geopolitical risk, not an unmanageable emergency.

Rebuttals

Side I Rebuttal: 70% crude diversification is progress, but LPG (~90% Hormuz-linked) and LNG remain highly exposed. SPR at only ~64% fill level and Moody’s explicit warning on India bearing the “maximum brunt” indicate buffers are insufficient for prolonged disruption. Rerouting works better for crude than for household LPG needs.

Side II Rebuttal: LPG pressures are being addressed via alternatives (e.g., US sourcing) and conservation. Successful vessel transits and increased Russian volumes show adaptation in real time, with no blackouts or mass shortages reported.

Final Synthesis Ultimately, the motion is largely valid for a prolonged blockade: critical vulnerabilities in LPG, limited SPR stocks, and macroeconomic transmission effects create a genuine energy security emergency, despite crude diversification gains. India has demonstrated resilience through rapid rerouting and buffers, but the crisis highlights the need to accelerate SPR filling, deepen non-Gulf ties, and fast-track the energy transition toward strategic autonomy.